Michigan’s segregated past – and present (Told in 9 interactive maps)

The words are startling to modern eyes.

Negro area. Old. Obsolete.

Shifting or infiltration: Jewish and Negro...

Negro homes all through the industrial area

Mixed poorer class...mostly laborers...Russian, Bohemian

These are U.S. government descriptions of neighborhoods in Kalamazoo, Detroit, Battle Creek and Pontiac in the 1930s, in language that makes it clear that “negro” homeowners were bad for real estate; that mixing races hurt home values, and that all-white neighborhoods needed protection from “lesser” populations.

How 'redlining' from the 1930s impacts housing patterns in 9 Michigan cities today:

African Americans and other minorities have long faced discrimination in the housing market – from real estate agents, landlords and sellers. The federal government became an active part of that discrimination in the 1930s when it began to explicitly use race and ethnicity to determine whether homebuyers were eligible for government-backed loans, in effect keeping some neighborhoods white and confining blacks and other minorities to less desirable areas of American cities. During the post-World War II boom in housing – and the wholesale creation of the suburbs – blacks received just 2 percent of all loans – despite representing 10 percent of the population – and typically only in areas where other blacks lived.

The maps that follow show how the Home Owners’ Loan Corp. (HOLC), created to save a housing market wracked by Depression-era foreclosures, helped deepen segregation in nine Michigan cities. We then show modern maps of those cities, to show to what extent the legacy of government-sanctioned segregation remains today.

Interactive maps:

Battle Creek

Bay City

Detroit

Grand Rapids

Flint

Kalamazoo

Muskegon

Pontiac

Saginaw

In identifying race, religion and ethnicity to help determine the creditworthiness of neighborhoods, the government made it near impossible for blacks and others to secure loans in “better” – mostly white – neighborhoods across Michigan. Government-sanctioned segregation also helped to shape areas of Bay City, Muskegon, Saginaw, Grand Rapids and Flint.

For anyone trying to understand why racial segregation persists today, the maps developed by the New Deal-era Home Owners’ Loan Corp. to stabilize the housing market reveal the active role government played, and its continuing legacy today, some eight decades later.

“(The maps) are the Rosetta Stone of the American city,” said LaDale Winling, an assistant professor of history at Virginia Tech, who was part of a project that has made the old HOLC maps available online. Winling and others argue that HOLC maps, along with decisions by its New Deal cousin, the Federal Housing Administration, help explain the location of predominantly black neighborhoods that remain in many Michigan cities today.

Recently, Detroit Mayor Mike Duggan made a similar presentation to the state’s most powerful business and political leaders at the Mackinac Policy Conference, when he pointed out government policies from the 1930s that still affect the city, region and state.

"There was a conscious federal policy that discarded what was left behind and subsidized the move to the suburbs," Duggan said, later adding: "This is our history, and it's something we still have to overcome."

Blacks were largely blocked from federally-backed mortgages, not because of their incomes or credit scores, but because of their race. The division of neighborhoods into good and bad ‒ white and black ‒ persists in many Michigan cities and regions, with the Detroit and Saginaw areas among the most segregated in the nation today. Indeed, the term “redlining” stems from using the color red on maps to indicate low-income neighborhoods or those with African-American or foreign-born populations.

The 1930s didn’t represent the first time blacks would face discrimination in housing, who had long felt the sting of racism from landlords, real estate agents and homebuyers.

But HOLC’s appraisals, combined with the Federal Housing Administration’s discriminatory racial policies, gave those slights a legitimacy that would endure for decades, and would delay integration of the suburbs.

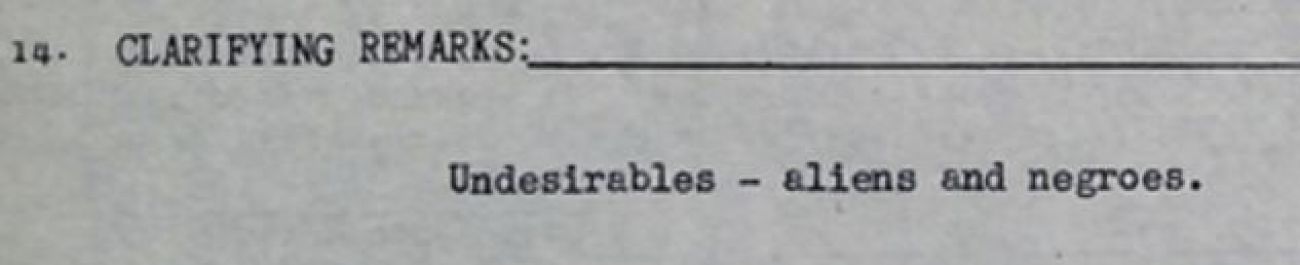

The language of government-sanctioned racism was perhaps most blunt in Flint. In one north Flint area, where 60 percent of residents were African-American and 40 percent foreign born in the 1930s, the HOLC appraisal made it crystal clear why it redlined the neighborhood:

“Undesirables,” the government appraisal read, “aliens and negroes.”

Historic but long-lasting

HOLC no longer exists and the FHA abandoned its race-based policies in the 1960s. But those policies locked in housing patterns and fostered the decades-long white flight that came to define regions like Detroit, establishing patterns that cannot be “undone” in a generation or two.

“If you were a white person buying a house in post-war America, you benefitted from this,” said David Freund, a professor at the University of Maryland whose 2007 book, “Colored Property: State Policy and White Racial Politics in Suburban America,” documented the role of HOLC and the FHA in cementing segregation.

HOLC was formed in 1933 and the FHA a year later. HOLC was created with the lofty purpose of helping lenders and borrowers crushed by the foreclosure crisis of the Depression by buying failing loans and extending the terms out over 10 to 15 years. The FHA would enlarge the government’s role by insuring new mortgages, greatly expanding the market by guaranteeing loans.

In the process, HOLC created its “residential security maps” to standardize appraisals across the country. The FHA, meanwhile, promoted segregation by pushing for areas to be of “the same social and racial classes.” The agency was leary of both “inharmonious racial groups” and “an incompatible racial element.”

To that end, the HOLC sought “inhabitant” data on how many “foreign-born,” “relief families” and blacks lived there. Another section noted whether was an “infiltration” of “undesirable” groups.

In addition to blacks, the presence of Jews, Poles and Italians are frequently mentioned under “infiltration.” These last groups did not suffer loan discrimination for as long as blacks.

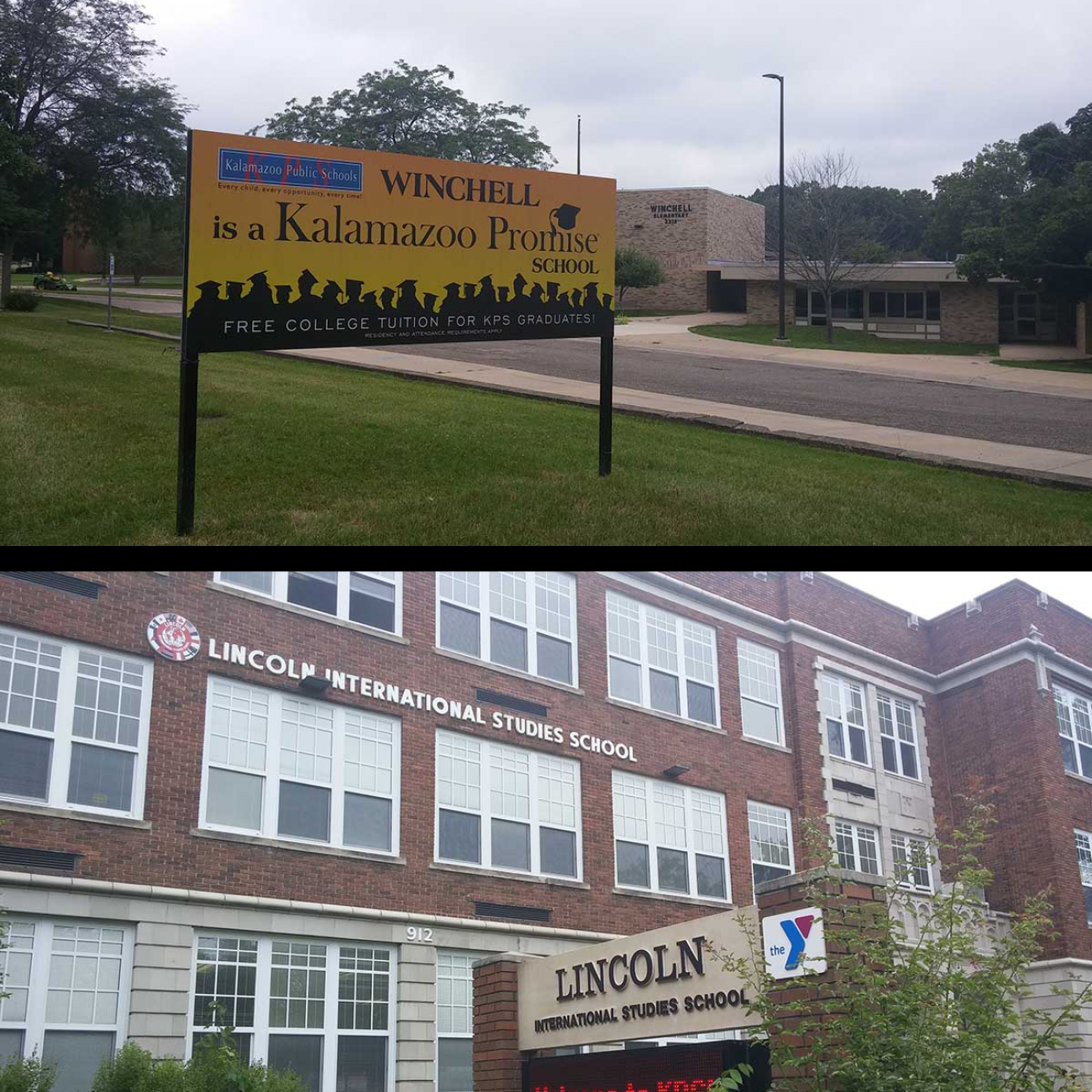

Kalamazoo, then and now

Driving around the neighborhood along Oakland and Winchell streets in Kalamazoo, you can see what the HOLC appraisers found attractive: nice homes on wide lots amid gently rolling hills. In the 1930s, it had something they also liked: it was all-white. No blacks or “foreigners” lived in the neighborhood.

It’s “favorable influences,” the HOLC noted, were transportation and good schools. And it was “restricted,” an indication by HOLC that deed restrictions on homes limited the neighborhood to whites only, Winling said. (The use of deed restrictions was first struck down by the U.S. Supreme Court in a 1948 decision.)

Today, the neighborhood is more integrated – roughly 10 percent of the population is black and a total of 20 percent non-white. But long-term investment in the neighborhood is telling, as are the schools.

At Winchell Elementary, just a third of students qualify for a subsidized lunch, compared with 62 percent across the entire Kalamazoo school district. And test scores are better as well: Compared with Lincoln International Studies elementary, about two miles north and east in a part of northern Kalamazoo that was deemed “hazardous” by HOLC, Winchell students performed far better, with double, triple and sometimes quadruple the percent of students proficient on state tests as those at Lincoln.

The Lincoln neighborhood in the 1930s was considered “hazardous,” a long-term risk for investment in part because it was nearby factories and congestion, but also because of the presence of “negroes” – which then comprised just 10 percent of population.

On the appraisal form, under the section “trend of desirability next 10-15 years,” the appraisers wrote: “Hazardous. Alien and negro labor.”

Today, the Lincoln neighborhood is overwhelmingly African-American and poor. But across town, where the green-coded Oakland and Winchell area was deemed “best” in 1937, decades of continuous investment are apparent on almost every block.

“They looked great then and they look great now,” said Winling, who is familiar with Kalamazoo having grown up in the area and attended Western Michigan University. “That’s (the) intergenerational effect of housing investment” ‒ investment that wasn’t available for much of the past century in the red-shaded areas of Kalamazoo.

Tim Ready, a sociology professor at Western Michigan University, is director of the Walker Institute for the Study of Race and Ethnic Relations. For the past decade he has worked to stem the racial divide in the city as the institute held seminars and programs highlighting Kalamazoo’s racial problems and sought solutions, including summer math and science camps for minority students in grades 3-8.

As he drove around the city recently, he pointed out the good neighborhoods and the struggling ones in a tour that could have been predicted by 80-year-old maps.

“I have a sense of indignation about it,” Ready said. “But it’s kind of my mission to address these issues.”

Wanting to cry

Born in 1959, Joyce Baugh grew up in segregated South Carolina and didn’t attend an integrated school until the state complied with desegregation efforts when she was in fifth grade. A professor of political science and public administration at Central Michigan University, she recalls being shocked at the segregation in the North when she came to Ohio to attend graduate school. An African American, she learned quickly it was a myth that only the South was segregated.

But it was years later, when researching a book on the landmark Milliken v. Bradley school desegregation case out of Detroit, in which the U.S. Supreme Court overturned a plan to bus students between Detroit and its suburbs, that Baugh saw the HOLC maps and read the neighborhood descriptions for cities across the country, not just the South.

“There are days you’re reading this stuff and you want to cry,” Baugh said.

Rejecting the criticisms of black leaders and others, HOLC and the FHA’s real estate economists put into federal policy what was then an accepted belief among whites, including academics: Home values could only be preserved if the races were kept separate. And even when separate, those neighborhoods with blacks were almost always considered the highest risk for investment and thus held the lowest value.

One neighborhood of Grand Rapids, just east of downtown, had several favorable factors, according to HOLC, including good access to transportation and good schools. It also had blacks – even “good” ones, apparently. “Negroes in area are of better type,” the HOLC appraisers wrote. It was still rated “hazardous” and shaded red.

The presence of blacks or “foreigners” weren’t the only reasons an area could get a “hazardous” rating. Neighborhoods across the country that lacked local zoning, paved roads and other urban infrastructure were downgraded. But while those things could change – city and rural leaders enact zoning regulations and improved infrastructure to secure higher FHA ratings and investment – people could not change their race, and the rules largely did not change in their favor.

In almost every area with even a handful of black families, the Home Ownership Loan Corp.’s residential security maps were colored red, meaning blacks could only get loans in segregated areas, and could not freely move beyond those areas with the aid of a government-backed mortgage, a benefit that was not denied to whites.

“Federal policy codified, sanctioned, and put tremendous force behind the theory that the mere presence of black people tainted a neighborhood and reduced its monetary value,” Freund wrote in “Colored Property.” “Meanwhile, selective credit programs created an economic environment that enabled whites to support racial exclusion while insisting, quite earnestly, that their preferences had nothing to do with prejudice.”

For all its exclusionary evils, HOLC and FHA’s entrance into the housing market was crucial to the explosion of home ownership nationally. While private loans at the time traditionally had to be paid off in five to six years, HOLC extended it to 10 and 12 years, an experiment that worked. Ultimately, the FHA would push the limit to 30 years and popularize the long-term mortgage we know today.

In Flint, the FHA insured tens of thousands of home loans for white families but only a couple dozen for blacks, many of whom had similarly good-paying jobs in the GM factories in town, said Andrew Highsmith, a professor at the University of California, Irvine, who studied Flint for his dissertation at the University of Michigan.

It has created neighborhoods that have consistently been eligible for millions in government support – and others that have not.

“That’s how you get from 1935 to 2017. This isn’t ancient history,” said Winling “These are long-term effects and they were intended as such.”

The policies, Freund argues, created a country in which whites gained access to the wealth-generating effect of homeownership that largely eluded blacks. It’s largely blamed for the substantial wealth gap that exists today, with white households having, on average, 12 times more wealth than the $11,030 the average black household has.

“The home is the single greatest investment a person can make,” Winling said, and for blacks, that home had to be bought largely in strictly defined areas. The idea of moving freely across a region was ridiculous to most blacks consigned by HOLC and the FHA to narrow strips of Detroit and other cities.

Finding solutions

Understanding the past, and it’s rough edges, is essential to solving lingering problems, Freund said, even if it makes people uncomfortable. ”I want people to make claims and fashion policies that are honest about this past,” Freund said.

That’s what made Mayor Duggan’s speech revelatory: As he pushes his administration to avoid the trap of “Two Detroits,” he’s doing so while acknowledging – and asking others to acknowledge – the past. (Admittedly, he’s also running for reelection against an opponent, Coleman Young Jr., who has hammered Duggan about the city’s “forgotten neighborhoods.”)

While lauding development in Midtown and Downtown, Duggan has repeatedly reached out to the city’s other neighborhoods, and his development “principles” call foran end to “economic segregation by pushing jobs into all neighborhoods.”

Altering long-term segregation has proven difficult. Some communities have tried, notably Shaker Heights, Ohio, and Oak Park, Illinois, a suburb of Chicago. And others are enacting and enforcing fair housing ordinances, offering home purchase assistance, promoting regional solutions to housing (requiring communities to set aside land for affordable housing) and experimenting with scattered site public housing, which has shown positive effects.

We live in the communities that we create. For most that means neighborhood block parties and attendance at the local PTA meetings. But it also means the policies that government enact. Fixing segregation by creating the cities of tomorrow may also take political action.

“You have to recognize and realize that if you want to change the current dynamic,” CMU’s Baugh said, “then you have to figure out public policy to address the problems.”

See what new members are saying about why they donated to Bridge Michigan:

- “In order for this information to be accurate and unbiased it must be underwritten by its readers, not by special interests.” - Larry S.

- “Not many other media sources report on the topics Bridge does.” - Susan B.

- “Your journalism is outstanding and rare these days.” - Mark S.

If you want to ensure the future of nonpartisan, nonprofit Michigan journalism, please become a member today. You, too, will be asked why you donated and maybe we'll feature your quote next time!